Home ownership is a strong part of Australia’s cultural identity, our way of life. That does not change when you retire…in fact, most Australian retirees prefer to continue living at home. And why not? Home is where you’ve raised your family, created memories, established yourself in a community.

Sadly, for many retirees, the need to fund 25-30 years of retirement leads them to sell the family home to downsize into a smaller home or unit, or retirement village. This often results in disruption and dislocation and doesn’t always deliver a financial advantage.

Australians want to stay at home

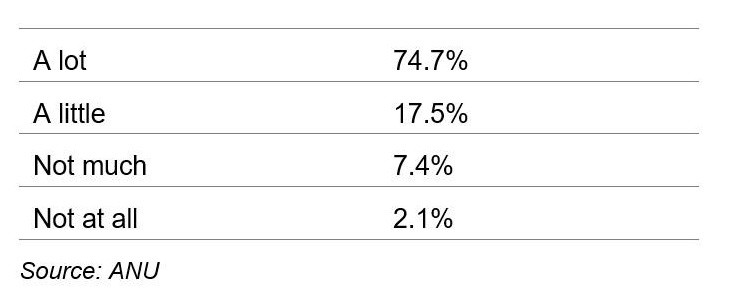

In 2017, researchers from Australian National University[1] polled over 2,500 Australians and found homeownership remains a national aspiration.

To what extent do you believe that owning your own home is part of the Australian way of life?

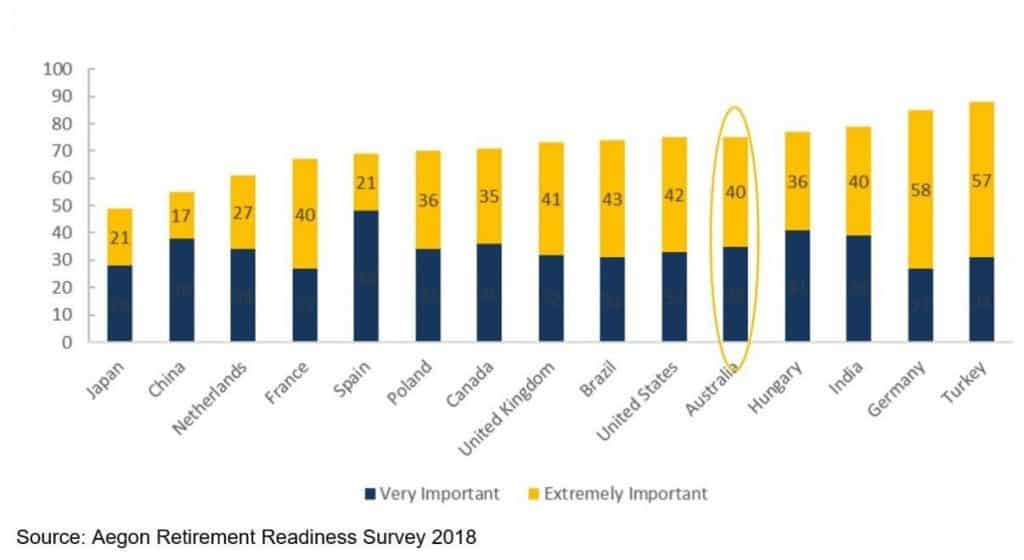

This has not changed in three years. According to the Confidence in Retirement Survey, conducted by Household Capital and Your Life Choices in December 2020, homeownership and retaining the family home remain important to older Australians.

The majority of Australian retirees own their own homes at retirement; despite government incentives to downsize it’s not the preferred option for most people. The survey referenced above found that the majority of retirees surveyed do not intend to downsize and, in the main, planned to modify their own environment and remain in their home for the rest of their lives.

As illustrated, Australians exhibit a strong intention to remain at home by comparative international standards.

The importance of staying at home in retirement

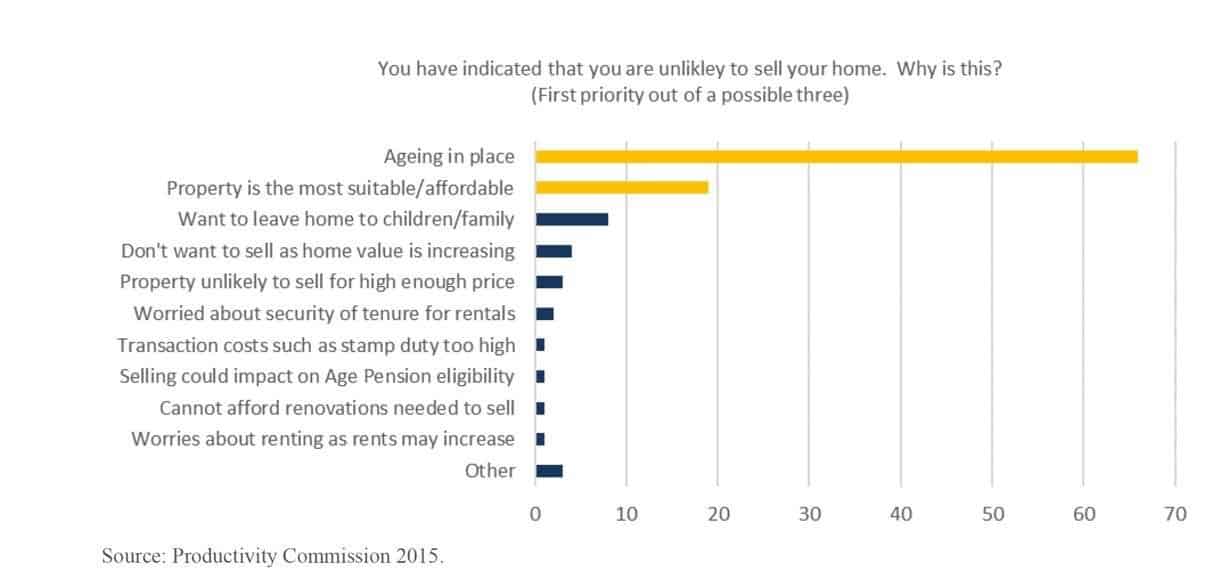

A Productivity Commission report[2] released in 2015 found that over 60% of older Australians would strongly prefer to ‘age in place’ by staying in their own homes. Over three-quarters, (76%) of over-60s told the Commission they want to see out their retirement in their own home, and 83% view homeownership as vital to maintaining independence and financial freedom as they age.

There are numerous benefits that arise from older Australians ageing in their family home:

- The familiar environment – research has shown people who age at home are happier and healthier

- Social networks – maintaining your social networks improves physical and mental health for older people who stay in their own home

- Adapt – you can modify your own environment to suit your changing needs.

The downside to downsizing

Selling the family home, moving to a lower-priced property and using the differential to fund retirement is often suggested as a major opportunity to improve access to home equity. Despite that, there are a number of downsides to consider:

- Costs – when you factor in legal and transaction costs, stamp duty and moving expenses, the realised value of downsizing is eroded.

- Availability – in many areas, there is limited availability of lower-priced accommodation, meaning that retirees may need to leave their community and social support structures to capture meaningful proceeds from downsizing.

- Suitability – downsizing options built on a single level are not always readily available; a new residence may mean stairs that challenge old hips and knees.

- Community – many people want to remain in their community, near their family and friends, with access to the services they frequently use. These may include medical and allied health practitioners, clubs and groups, the library and even a favourite café.

- Centrelink impact – importantly, despite recent downsizing concessions for retirees, tax and transfer systems result in assets released from home equity downsizing having a potentially adverse impact on assets and income tests for access to the Age Pension.

- Complex and disruptive – despite government incentives for older Australians to downsize, it’s not that easy.

The Productivity Commission report found that age-specific housing such as retirement villages are very expensive and limited in number and location. On top of that, retirement village fee structures are regulated in a way that makes them overly complex and difficult to compare.

Although most Australians want to age at home (see above), longer lives combined with retirement funding inadequacy may result in retirees being forced to prematurely downsize or relocate to retirement homes with significant disruption and financial disadvantage.

More importantly, in-home poverty, forced downsizing or premature relocation to aged care can undermine the lifestyle and wellbeing of retirees and the economic burden of retirement. Approaches that can help Australians remain at home and meet the challenges of both longevity and retirement funding adequacy will play an important role in meeting the needs of many older Australians into the future.

[1] ANU poll of Attitudes to Housing Affordability, March 2017

[2] Housing Decisions of Older Australians, Productivity Commission, 2015

Household Capital Pty Limited ACN 618 068 214 is the issuer of the information on this website. Household Capital Pty Limited ACN 618 068 214, Australian Credit Licence 545906, is the Servicer for the credit provider Household Capital Services Pty Limited ACN 625 860 764. HOUSEHOLD CAPITAL, HOUSEHOLD TRANSFER, LIVE WELL AT HOME and the Star Device are trademarks of Household Capital Pty Ltd

SHARE THIS PAGE

You may also like