Australia’s retirement income policy has been traditionally framed as having three pillars: superannuation, the Age Pension and other savings. For the first time, the Australian government included home equity in that third pillar in its terms of reference for its Retirement Income Review. For many self-funded retirees, the current environment has hit major sources of income: dividends, rental income from residential or commercial properties and cash.

At the same time, most super funds finished the 2020 financial year flat. Increasing drawdowns in this environment isn’t optimal, as it will take growth and time to recover – and it’s much harder to get growth from a diminishing pool of capital that’s being drawn down to supplement lost retirement income.

Home equity is one way to improve retirement funding while leaving super accounts to recover. It’s not only the current situation to consider – Australians are experiencing a major societal transformation with millions of baby boomers reaching retirement. Around 5.5 million people born between 1946 and 1964, will need long term funding. While we are living longer than ever, this presents a real conundrum – many simply don’t have sufficient savings to fund a comfortable retirement for their projected lifespan.

Living longer, not necessarily better

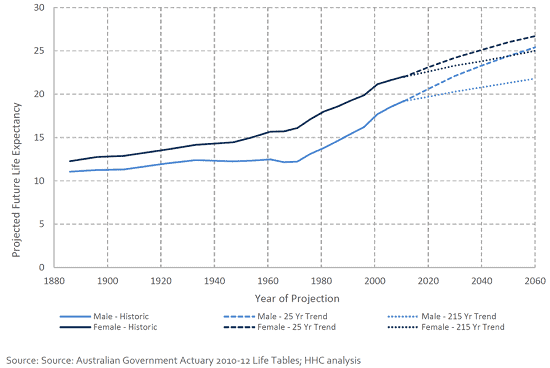

The life expectancy of Australians in retirement has almost doubled in the last 150 years thanks to better lifestyles and medical breakthroughs. Since the introduction of compulsory superannuation in 1992, Australians at retirement have gained an extra decade of longevity – and an extra decade to fund. Figure one shows the range of expected increases in longevity after retirement for Australian men and women based on current assumptions. It is estimated that retirees aged 65 now will live on average until 84 for men and 87 for women.

The blessing of longevity is a new and extended phase of life that will endure well past 90 for many people. The curse is that your clients need to plan for 25-30 years of retirement.

Super alone is not super enough

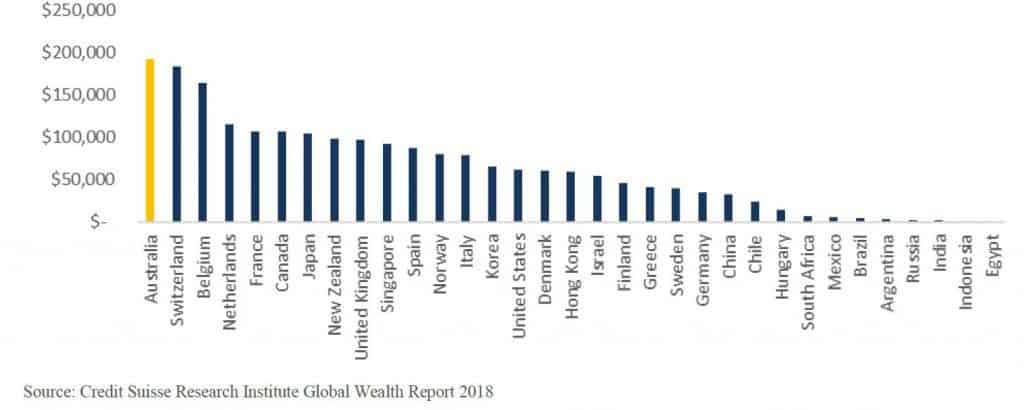

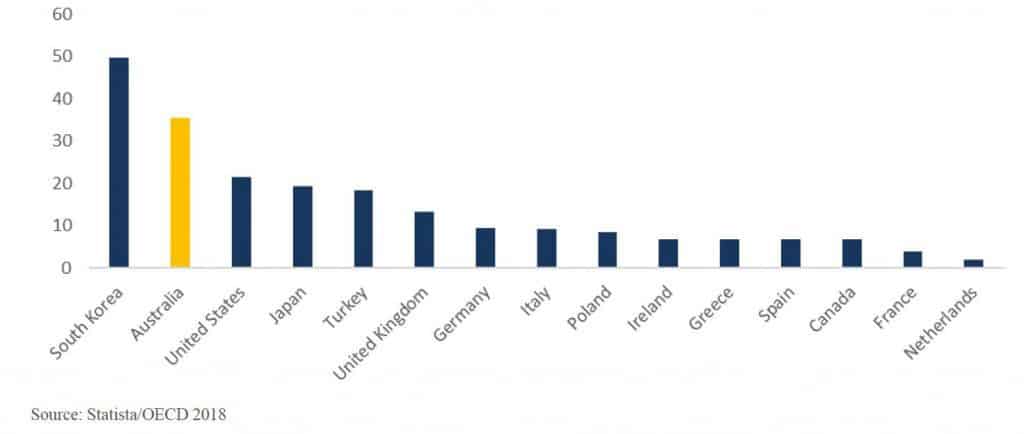

Despite high total median wealth (figure two), retired Australians experience high levels of relative poverty (figure three).

To enjoy more good years of life in retirement, adequate resources are required. The Australian superannuation system was designed to supplement the Age Pension with private, account-based savings from wage contributions. For many retirees, the introduction of superannuation contributions occurred only part-way through their careers at lower levels. The 3% annual contribution in 1987, followed by the Superannuation Guarantee increasing to 9% by 2002, has led to a major shortfall in available assets to fund retirement. Baby boomers also missed out on the benefits of compounding returns over time.

According to ASFA1, Australians aged between 60-64 are retiring with a median balance of $154,453 for males and $122,848 for females, compared to a targeted retirement balance of $545,000 (ASFA Comfortable Retirement Standard). This inadequacy of superannuation savings to support a quality retirement lifestyle is a major challenge.

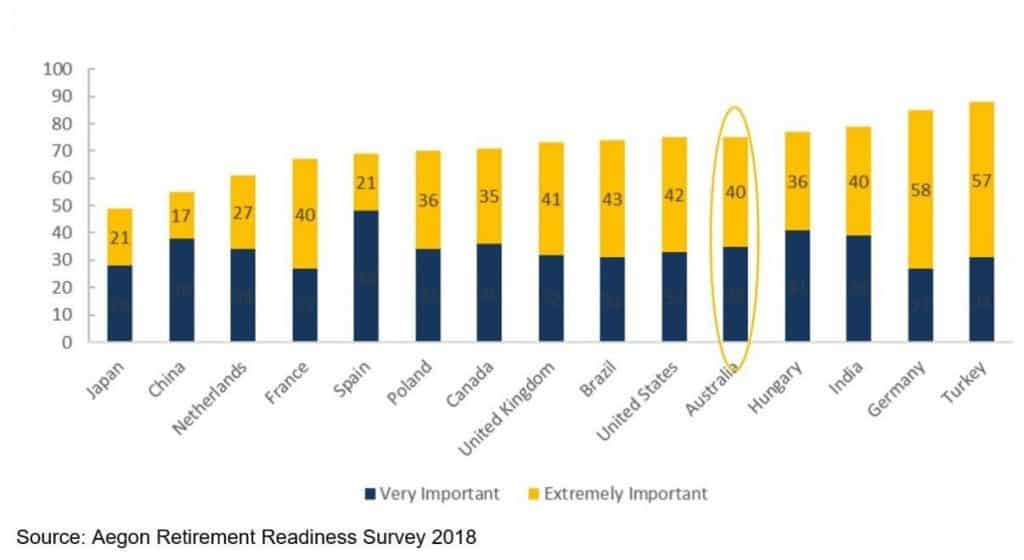

For most Australians, the majority of their wealth is tied up in their home equity; in total, there is more than one trillion dollars in untapped home equity owned by Australian retirees 2. Long, healthy lives enable Australians to spend a greater part of their retirement living independently. Most retirees wish to stay in their own home as they age, as illustrated by figure four, and their untapped savings are a valuable resource that could be utilised to provide improved retirement funding.

The poor outcomes for residents of aged care facilities during the COVID-19 pandemic, coupled with findings from the Aged Care Royal Commission, are likely to increase the desirability of remaining in the family home for as long as possible.

The family home versus super

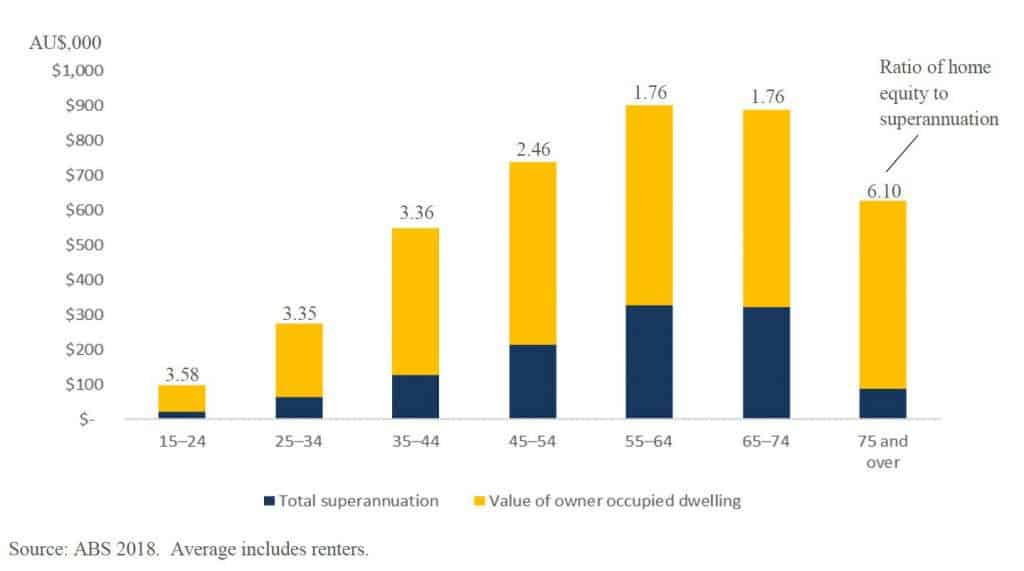

Figure five shows the total average superannuation versus home equity for Australian households during the course of work and retirement. Within 10 years of retirement, superannuation savings are largely depleted.

For Australian homeowners at retirement, the average household home equity is typically almost twice the value of superannuation. By the time retired cohorts have reached 75+ years of age, home equity savings have grown to over six times the value of superannuation.

On average, Australians’ superannuation lasts about 10-15 years after which many Australians in retirement can expect a further 10-15 years of underfunded or inadequate retirement supported by the Age Pension.

Assets, income and contingency funding

Many economists and superannuation executives continue to ask, “Why do retirees die with so much wealth left in super?” The simple answer is that accessible savings in superannuation are Australian retirees’ main way to manage both contingency funding and longevity risk. No-one can tell when they will die or the major expenses they may incur along the way. While retirees do draw down their super and retain a contingency buffer, they also die with far too much wealth tied up in their homes.

Currently, retirees have no ability to transform the adequacy of their retirement resources to responsibly access their accumulated wealth throughout retirement. To do that, we need to consider ways to provide access to the largest pool of savings for most Australian retirees – their own home equity.

How can home equity improve retirement funding?

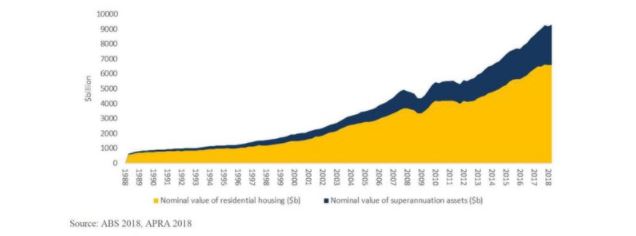

Australian retirees are already disproportionately exposed to residential property. Throughout the expansion of the Australian superannuation system since 1988, residential property has been a vastly larger national asset class (figure six).

For many baby boomers at or in retirement, the majority of their lifetime savings are held in a single residential property. Indeed, residential property remains the most significant store of wealth for Australian households, despite the introduction of superannuation.

For the past 20 years – and in many cases since baby boomers bought their first homes – Australian residential property has provided strong returns with no greater volatility than other investment asset classes.

Recently, most major residential property markets have experienced a major cyclical correction, putting residential property baselines in place. New approaches for widespread access to home equity are timely – the equity of both lenders and the large cohort of baby boomers approaching retirement will be protected in the long term; as valuations increase, so will access to equity. With the family home being a major store of household wealth, now is the time for responsible and sustainable access to home equity.

Home equity retirement funding

Facilitating access to home equity to fund long-term retirement needs represents an opportunity to meet a major unmet community need and provide a sustainable fiscal stimulus to enhance economic growth.

Household Capital identifies a range of responsible retirement funding needs which may be met with access to home equity. Two guiding principles govern this approach. First, long-term retirement funding needs are largely met by the transfer of home equity to appreciating assets which can meet those funding needs over time. Second, credit is constrained for short-term consumption of home equity or deployment to depreciating assets.

The integration of home equity with Australia’s retirement income system is likely to be one of the outcomes of the government’s Retirement Income Review, due to report in the second half of 2020. Home equity should form part of long-term retirement planning; it should be integrated within the Australian financial advice and superannuation sectors to make it widely available to support retirement funding.

Introducing the Household Loan

Household Capital is a specialist retirement funding provider that provides responsible long-term access to home equity to meet the needs of an aging population. We work with advisers to help your clients improve their retirement lifestyle by enhancing retirement income (Home Income), providing access to capital and improving retirement housing.

We aim to provide retirees with the best of both worlds – to continue living in their family home with the confidence to enjoy the retirement lifestyle they deserve.

Our Household Loan is an innovative type of reverse mortgage that’s been designed to meet the needs of Australian retirees and work within Australia’s retirement system. For clients aged 60+, it allows them to access a portion of their home equity. This may be to meet shorter-term needs in the current environment, or as part of a longer-term retirement strategy.

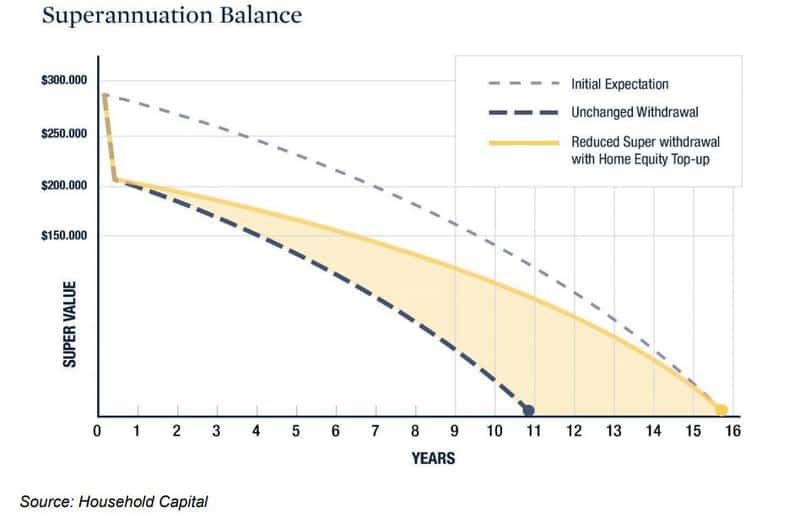

Case study: Reducing super drawdowns to increase its longevity

The following case study demonstrates how reducing super drawdowns with an income boost from a Household Loan can make a significant difference to how long a client’s super lasts.

Peter and Helen are a 65-year-old couple with $280,000 between them in super and a house they own outright that’s valued at $900,000. The couple draw an income of $2,000 a month from their super and receive $2,847.20 a month from the pension.

They want to ensure their super lasts as long as possible, so are keen to keep it invested so they can benefit from a stockmarket recovery. At the same time, they don’t want to sacrifice the retirement lifestyle they worked hard to achieve.

If Peter and Helen keep drawing a monthly income of $2,000 from super, their super runs out by the time they’re 75 and they’re down to living on the pension alone. If they cut their expenses and reduce their monthly super income to $1,500 a month, their super lasts until they’re 80.

But if they reduce their monthly super income to $1,500 and top it up with a $500 monthly Home Income payment, they can still stretch their super out until they’re 80 but maintain their current lifestyle.

This does not require a significant amount of their home equity; it requires a $90,000 Household Loan. The sum repayable at the end of the 15-year loan term would be about $136,000 in total due to compounding interest – not a large bite out of the couple’s total home equity of $900,000 (and that’s assuming their home doesn’t increase in value at all over the 15 years).

You can see in the chart below how a Household Loan can help super last for longer (and that’s assuming their super investments don’t increase in value at all over the 15 years either).

Clear benefits can be found in an approach that includes the responsible use of home equity. Existing financial services infrastructure is used. It is the most efficient way to ensure long-term planning for retirement funding. Home equity can be deployed in appreciating assets managed by the distribution partner to generate long-term retirement income.

By restructuring responsible access to home equity, retirees receive multiple benefits:

- Access to savings: where the majority of lifetime savings are in the home, these are now available to improve retirement funding.

- Improved retirement funding: where the Age Pension and superannuation are inadequate, home equity can improve retirement funding.

- More reliable retirement income: for some retirees, income may be volatile relative to the performance of superannuation. Home equity can smooth income and capital supply.

- Asset diversification: as superannuation is depleted, retirees’ assets become increasingly concentrated in a single residential property. Transfer to superannuation can diversify assets.

- Long term financial advice: higher super balances during retirement can qualify for longterm financial advice and the benefits that come from holistic management of household savings.

- Sequencing risk management: responsible, long-term access to home equity adds a second, independent, largely uncorrelated source of income should super assets decline periodically.

Increasing longevity and impacts on the value of financial assets and superannuation from the current crisis suggests it’s an optimal time to include home equity as a part of retirement planning. By drawing on multiple sources of income, Australian retirees can achieve funding adequacy throughout the full course of 25+ years of retirement. However, to achieve this, retirees must be able to responsibly and cost-effectively access home equity savings to generate retirement income.

Applications for credit are subject to eligibility and lending criteria. Fees and charges are payable and terms and conditions apply (available on request). Household Capital Pty Limited is a credit representative (512757) of Mortgage Direct Pty Limited ACN 075 721 434. Australian Credit Licence 391876.

SHARE THIS PAGE