3 February 2021

Questions to ask before you step in as Bank of Mum and Dad to fund your kids getting into the property market.

Parents planning to help their children into the property market face tough decisions that could jeopardise their financial welfare and family relationships if not handled carefully.

Rising divorce rates, soaring property costs, complex tax issues and the prospects of rising borrowing rates are making the choice of choosing between a loan, gift or inheritance to fund a purchase even tougher.

For fathers such as Nigel Smart, the key issues were helping his adult son and daughter in a way that both considered equitable without jeopardising his financial future.

Smart, a retired consultant who studied astrophysics and lives in Balwyn, about 16 kilometres north-east of Melbourne, decided to contribute to a house deposit for his 44-year-old son, daughter-in-law and three grandchildren aged between 11 and five years.

“I’m in a reasonable financial position, and I’ve made it clear to my daughter that there is a quid pro quo, or a favour returned to even any advantage for her brother,” he says.

Parents such as Nigel are aware of the crippling burden their children face saving a deposit and then paying for a mortgage while raising a family, particularly in Melbourne and Sydney.

New homebuyers in Sydney are taking almost 17 years to save a 20 per cent deposit for an average house and spending more than 60 per cent of their household income repaying the mortgage, according to a survey by the ANZ CoreLogic Housing Affordability report.

Sharply rising property costs mean that many children are forced to buy properties long distances from their parents and have to delay starting families until they reach their saving goals.

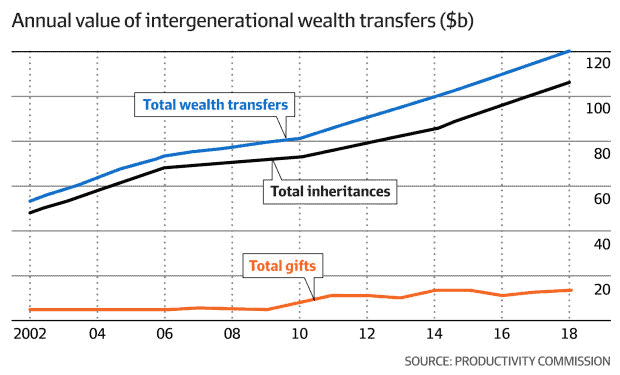

Transfers from cashed-up property-owning parents have more than doubled in real terms since 2001 to more than $120 billion a year and are expected to top $224 billion a year by 2050, according to the Productivity Commission.

But parents face tricky tax, legal and emotional issues balancing their welfare and wishes with those of their children, grandchildren and other relatives, particularly if there are marriage breakdowns.

Here are the key “Bank of Mum and Dad” questions to ask when considering helping children buy a home.

What happens if I make a gift?

Parents annually give about $12 billion in property, cash and cars to their children, or about three-times more than 20 years ago, according to the Productivity Commission.

Mark Chapman, tax director at H&R Block, says: “If you are simply giving cash, there are no tax implications for either the giver or receiver. But for other types of assets such as property, capital gains tax may need to be considered.”

A property given to children – or other family members – will be deemed to have been disposed of at its market value, “which could trigger a hefty CGT bill” for the parents at the time of transfer, Chapman adds.

“Those who gift their home may be able to use the main residence exemption to reduce, or eliminate, their CGT.”

Chapman says it is crucial for anyone giving a property to know its market value on the date of the gift.

Paul Moran, a financial adviser and principal of Moran Partners Financial Planning, warns those considering a gift must do the calculations to ensure they have enough left over for their retirement.

“While there is no rule against gifting in Australia, benevolent parents need to remember to look after themselves first,” says Moran.

“One problem we see is that gifts are often made after a period of good performance in financial markets and this lulls the ‘gifters’ into thinking that returns will be above average forever. This can lead to great disappointment and sometimes excessive risk-taking to try to make up the extra income.”

What are the implications of helping with a loan?

Parents and family can assist their children buy a property through a loan towards a deposit, acting as a guarantor for a bank loan, helping with mortgage repayments or being a joint home loan holder.

Industry specialist Chris Foster-Ramsay, principal of Foster Ramsay Finance, says parents with memories of the 1980s’ property market crash scrutinise loan terms more closely – whether from the bank or family.

That’s because a spate of recent court cases reveal a poorly executed loan can jeopardise parents’ financial security, divide families and result in wealth being transferred to the wrong parties, such as a child’s estranged spouse.

Foster-Ramsay says helping with a loan is better than a gift because if there is a relationship breakdown between their offspring and a partner or spouse, there could be a legal claim on the gift.

Michael Krivohlavy, a father of four from Kareela, which is 20 kilometres south of Sydney, is releasing equity in his home to raise funds for his children’s properties.

Krivohlavy, who sells development sites, adds: “It’s wise to get them involved in the property market and get them started buying their own properties. But I don’t want them living somewhere ‘back of Bourke’ because it’s the only place they can afford. If I help them financially, they can live closer to me.”

Key issues include:

- All parties taking independent legal advice to be aware of legal rights and obligations before they sign any loan guarantee documents.

- Parents specifying in their wills whether the debt will be forgiven and ensuring that other beneficiaries will not be disadvantaged.

- Being aware of any loan agreement with the bank (including repayment conditions, interest rates and the lender’s rights on default).

- Where there is a default on a loan between parents and offspring, lawyers warn that courts could consider it a sham and parents will lose out.

- Specify whether any loan guarantee is partial or full. A partial guarantee, of say, the first 20 per cent of a loan reduces exposure and limits risk. Advisers warn a loan will affect parents’ borrowing capacity and could be costly to unwind because of potential CGT and stamp duty.

- When standing guarantee on a loan, shop around for the best rates and conditions. The accompanying table shows top market rates, but terms vary between borrowers.

- Include an exit clause if you’re providing a loan for a deposit to your child, and regularly review the arrangement. His or her rising income might enable the loan to be refinanced earlier.

“A cash loan is tax-free because in effect nothing is given away – the cash is gifted, but the borrower in effect has to repay it down the track,” says Chapman.

“If the loan is interest-free, there is no taxable income from the loan. If the loan is interest-bearing, the interest has to be reported as income.

“If the lender is concerned that the borrower is going to squander the loan – for example, through drugs or a poor choice of relationships – then the lender has the option to increase the interest rate. Obviously, this will be taxable income, but the lender is at least getting something back.”

Parents such as Krivohlavy are using the growing equity in their family homes to fund equity release agreements, which allow the homeowner to sell a portion of the value of their home for a lump sum, or instalments.

Joshua Funder, Household Capital’s chief executive and founder, says: “Transferring home equity to future generations for first-time home deposits, paying off children’s mortgage or funding children’s education is giving with living hands when recipients need it most.”

Those considering the government or private-sector release schemes should consult an experienced financial planner because terms, rates and conditions vary between providers.

What happens if my child’s relationship breaks down?

The number of divorce settlements, which typically involve division of family homes, is being pushed even higher by fallouts caused by COVID-19, say divorce lawyers.

This is contributing to many parents and other testators taking more control over loans and gifts because they are concerned about relationships within families, such as claims from estranged spouses of their children.

Anna Hacker, national manager, estate planning at Australian Unity, says most parents are considering some form of trust – up from about 70 per cent in the past 20 years – to ensure tax efficiency and improve control.

What family conversations do we need to have?

An effective and simple way to defuse future bombshells, such as legal actions, is for parents to discuss with family members why a loan might be made to one child and not another.

Dianne Cuka, EY Oceania private tax leader, says it is “important and sensible” to discuss deals with siblings “so that misunderstandings can be addressed and issues can be discussed in an open and transparent manner. Get everyone on the same page”.

That also includes making sure any future distributions are equitable by taking into account the rising value of some assets, such as a family business or property, or other siblings not being given a parental loan, she says.

Are there any Centrelink implications?

Brendan Ryan, principal of Later Life Advice, an independent financial adviser, says there is a limit on gifts of $10,000 in one financial year and $30,000 over five years before it affects Centrelink payments.

Jointly buying a property with a child to protect a financial contribution from marriage break-up, or to reclaim the money later, can also be used by Centrelink when assessing benefits, Ryan warns.

“Being a part owner of the house that rises in value could result in a taxable gain for the parents and the loss of an opportunity for tax-free growth for the child,” he warns.

“Also, any increase in value may also be assessable for Centrelink purposes when looking at age pension eligibility.”

Original article found at the AFR

Household Capital Pty Limited ACN 618 068 214 is the issuer of the information on this website. Household Capital Pty Limited ACN 618 068 214, Australian Credit Licence 545906, is the Servicer for the credit provider Household Capital Services Pty Limited ACN 625 860 764. HOUSEHOLD CAPITAL, HOUSEHOLD TRANSFER, LIVE WELL AT HOME and the Star Device are trademarks of Household Capital Pty Ltd

SHARE THIS PAGE